On the one hand, on the other hand....

January 19, 2023

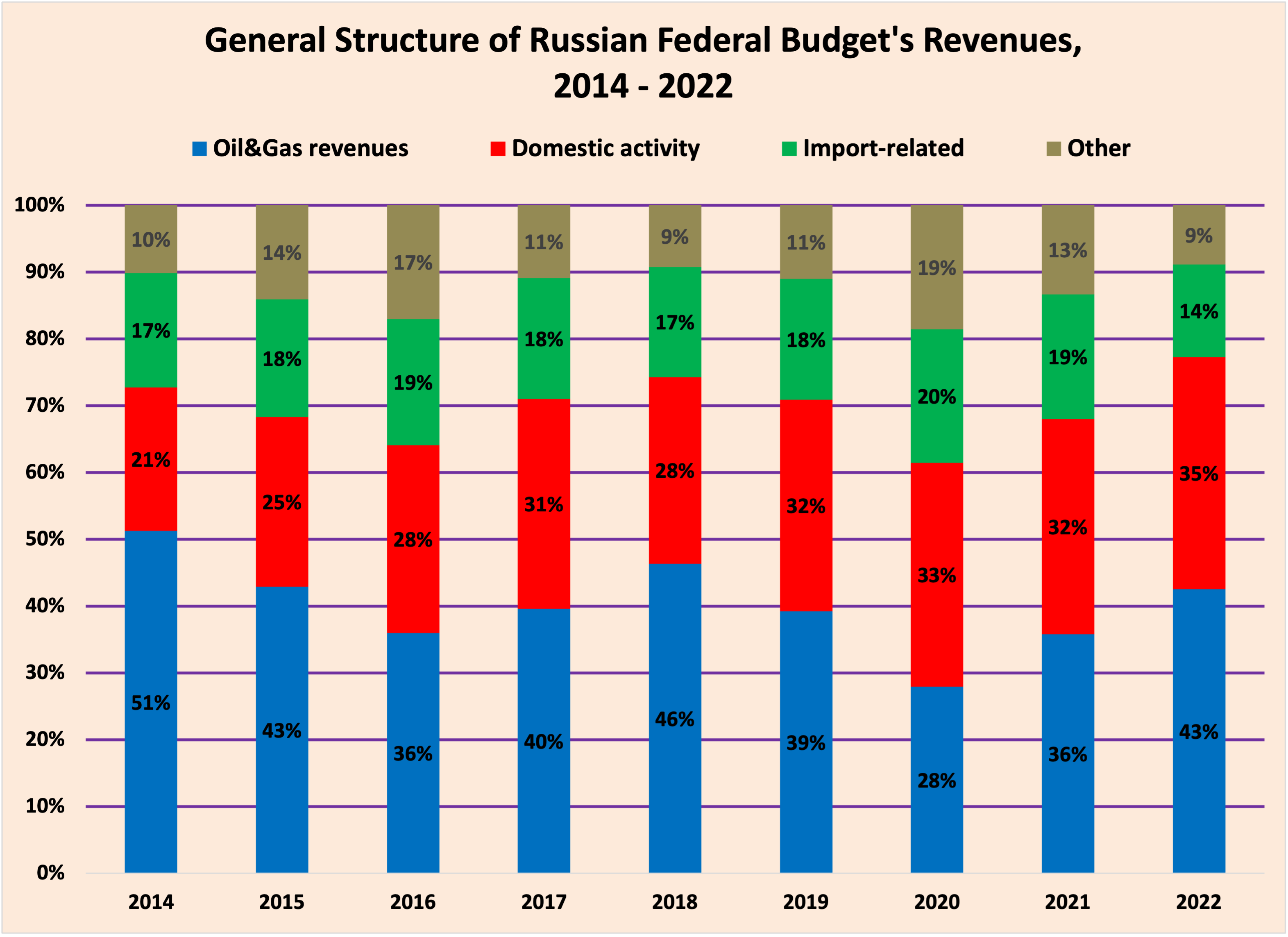

The summary results of the federal budget execution for 2022 published by the Ministry of Finance (revenues by category, expenditures, and deficit in one line) do not look unexpected and, at first glance, reflect the picture of the state of the Russian economy.1 Total budget revenues increased by 10% compared to 2021, with oil and gas revenues up 28%, revenues related to domestic production (VAT, excise taxes, income tax, and personal income tax) up 18%, and revenues related to imports down 20%.

The share of oil and gas revenues rose to 43% (the average level of 2015-2018)—i.e., at first glance, the budget’s dependence on the situation in commodity markets has increased. However, the intra-annual breakdown of oil and gas revenues, cleared of the extraordinary tax on Gazprom, which brought 1.45 trillion rubles in the last three months of the year (more than 5% of annual budget revenues), clearly demonstrates that the primary growth of oil and gas revenues occurred in January-May, after which the effect of Western sanctions cannot be overlooked—the average monthly “cleared” oil and gas revenues in the fourth quarter was two times lower than in the first five months of the year.

At the same time, the dynamics of revenues related to domestic production developed in precisely the opposite way: The volatile dynamics of VAT revenues (the tax that best reflects domestic economic activity) in April-July was replaced by their confident growth in autumn. The reason for such a U-turn does not require much searching: Starting from the middle of the year, the Finance Ministry sharply increased military budget expenditures (including spending on the Federal Guard Service and the Pension Fund, financing compensation payments to families of the dead and wounded), which in total exceeded the level specified in the law by no less than 2 trillion rubles ($29 bln.).

The most essential budget information was the report on using funds from the fiscal reserve, the National Welfare Fund, which dealt a heavy blow last year. In general, the size of the NWF decreased by 3.1 trillion rubles (23%). At the same time, its liquid part (what can be used to finance budget spending without any problems) decreased more, by 2.3 trillion rubles (27%), amounting to 6.13 trillion rubles at year-end ($87.2 bln., 4.6% of GDP). Given that the 2023 budget deficit is planned at 2.9 trillion rubles ($42 bln., 2% of GDP), and the Ministry of Finance plans to finance it in full at the expense of the National Welfare Fund, we can say that the bottom is starting to show at the Ministry of Finance “piggy bank.”2

It is important to add that about 40% of the reduction in the liquid part of the NWF (more than 900 billion rubles) last year was not connected with the financing of the budget deficit but was caused by the financing of extrabudgetary expenses: The purchase of bonds of Russian Railways, the purchase of shares of Aeroflot and Gazprombank, bonds of private airlines, placement of NWF resources on deposits in VEB, VTB, and Gazprombank. From the view of budget statistics, such transactions are not expenses; they are reflected as replacing liquid assets with illiquid ones. Given that in 2023 the government plans to continue this practice (at least, it is known about the intention to allocate 175 billion rubles to finance the purchase of Superjet aircraft for Aeroflot), the accumulated reserve may completely disappear by 2024.

The Ministry of Finance has not given any breakdown of expenditures, so this part of the budget cannot be discussed yet. Moreover, according to Finance Minister Anton Siluanov, in December the government started financing next year's expenses. We can only assume that these expenditures were related to the financing of arms production, but it is impossible to make any quantitative estimates.

About 40% of the illiquid part of the NWF are shares of Sberbank, which have lost more than half of their value over the year. In this connection, the change in the value of the illiquid part of the NWF is largely due to fluctuations in the quotations of Sberbank shares, as well as changes in the ruble exchange rate (the latter also applies to the liquid part of the NWF).